What is Carbon Accounting?

Carbon accounting, also known as greenhouse gas (GHG) emissions accounting, is a technique used by analysts to understand the extent of an organization’s carbon emissions. It calculates the amount of carbon dioxide emissions a business produces, both directly and indirectly. Governments, businesses, and individuals can all use carbon accounting to calculate their GHG emissions.

Microsoft for instance, has made their sustainability efforts well known via the use of carbon accounting, such as having pledged to become carbon negative by 2030 by using extensive carbon accounting measures to monitor and reduce their emissions.

By accurately accounting for their carbon emissions, organizations can set reduction targets, develop operations decarbonization and emissions offsetting strategies, while improving overall sustainability performance. It is a critical step towards mitigating climate change and fostering transparency in corporate environmental responsibility.

How to Complete a GHG Inventory?

Accurate GHG inventories are the foundation for effective emissions management, reporting, and climate action. If you are looking to leverage carbon accounting, then you’ll have to learn how to prepare a GHG inventory:

Accurate GHG inventories are the foundation for effective emissions management, reporting, and climate action. If you are looking to leverage carbon accounting, then you’ll have to learn how to prepare a GHG inventory:

- Plan: Choose a base year and determine the organizational and operational boundaries. Identify activity data and choose methodologies.

- Collect Data & Quantify Emissions: Gather the data needed to quantify GHG emissions. You can do this by developing data collection tools and compiling facility data. Thereafter, choose emission factors and calculate emissions.

- Develop a GHG Inventory Management Plan: Create an Inventory Management Plan (IMP) to formalize the process for collecting, calculating, and maintaining GHG data.

- Create a Report: Write a Sustainability & ESG report which includes your GHG inventory while documenting methodological approaches.

- Review: Review improvement options, discuss lessons learned, and develop an improvement plan.

What’s Difficult to Estimate with Carbon Accounting?

Carbon footprint uncertainty refers to the margin of error or imprecision in estimating the carbon footprint compared to the real value. The uncertainty of each emission item therefore occurs both in terms of activity data and at the level of the associated emission factor.

There are many things that cannot be measured in carbon accounting, including:

- Emissions Linked to a Specific Process: When emissions linked to a specific process cannot be measured, another process that is similar is used to model them.

- Emissions Specific to a Study Area: If emission data or factors are not specific to the study area, they cannot be used.

- Emissions from Products: When using a spend-based emission factor, the product is only categorized as furniture, not the specific chair or table.

What are the Most Popular Calculation Methods to Measure GHG Emissions?

An organization’s GHG emissions can be calculated using various methodologies. The chosen calculation method plays a crucial role in determining the accuracy and reliability of the emissions data in hand. This in turn helps organizations to understand their impact and address concerns regarding reducing emissions.

- Spend: The spend based method calculates carbon emissions by considering the financial value of a purchased good or service and multiplying it by an emission factor. It is an indirect method because you are not calculating your emissions of specific activities, but you rather calculate the emissions based on money spent on a good or service.

- Activity: The activity-based method places a detailed focus on the company’s overall operations enabling a more accurate quantification of the resulting carbon emissions. The activity-based method multiplies the physical unit of an activity by its corresponding emission factor. From manufacturing processes to vehicle use, it identifies specific emission sources, guiding targeted reduction efforts. For example, the number of litres of fuel burned is multiplied by the emission factor for fuel.

- Hybrid: The hybrid methodology, recommended by the Greenhouse Gas Protocol (GHGP) and widely adopted by organizations, combines the strengths of both spend based and activity-based approaches. This method entails collecting as much activity-based data as possible from the value chain and supplementing it with spend based estimates for the remaining emissions. The hybrid approach offers a balanced and comprehensive assessment of an organization’s carbon footprint while maximizing data accuracy and minimizing gaps in emissions reporting.

What is CO2e?

CO2e, or carbon dioxide equivalent, is a standardized unit used to measure and compare the impact of different greenhouse gases (GHGs) based on their global warming potential (GWP). Since not all GHGs have the same warming effect, CO2e helps express their impact as an equivalent amount of carbon dioxide (CO₂), the most common greenhouse gas. Each GHG has a GWP assigned to it over a specific time period (usually 100 years), which indicates how much heat it traps in the atmosphere compared to CO₂.

For example:

For example:

- Carbon dioxide (CO₂) has a GWP of 1

- Methane (CH₄) has a GWP of 25

- Nitrous oxide (N₂O) has a GWP of 298

This means that 1 ton of methane has the same climate impact as 25 tons of CO₂, and 1 ton of nitrous oxide equals 298 tons of CO₂ in terms of global warming effect.

Illustratively, if a company emits:

- 2 tons of CO₂

- 0.4 tons of CH₄

- 0.1 tons of N₂O

Then, CO2e = (2 × 1) + (0.4 × 25) + (0.1 × 298) = 2 + 10 + 29.8 = 41.8 tons CO2e

Such measurement enables companies, governments, and organizations to track, report, decarbonize operations and reduce total climate impact more effectively in a standardized way.

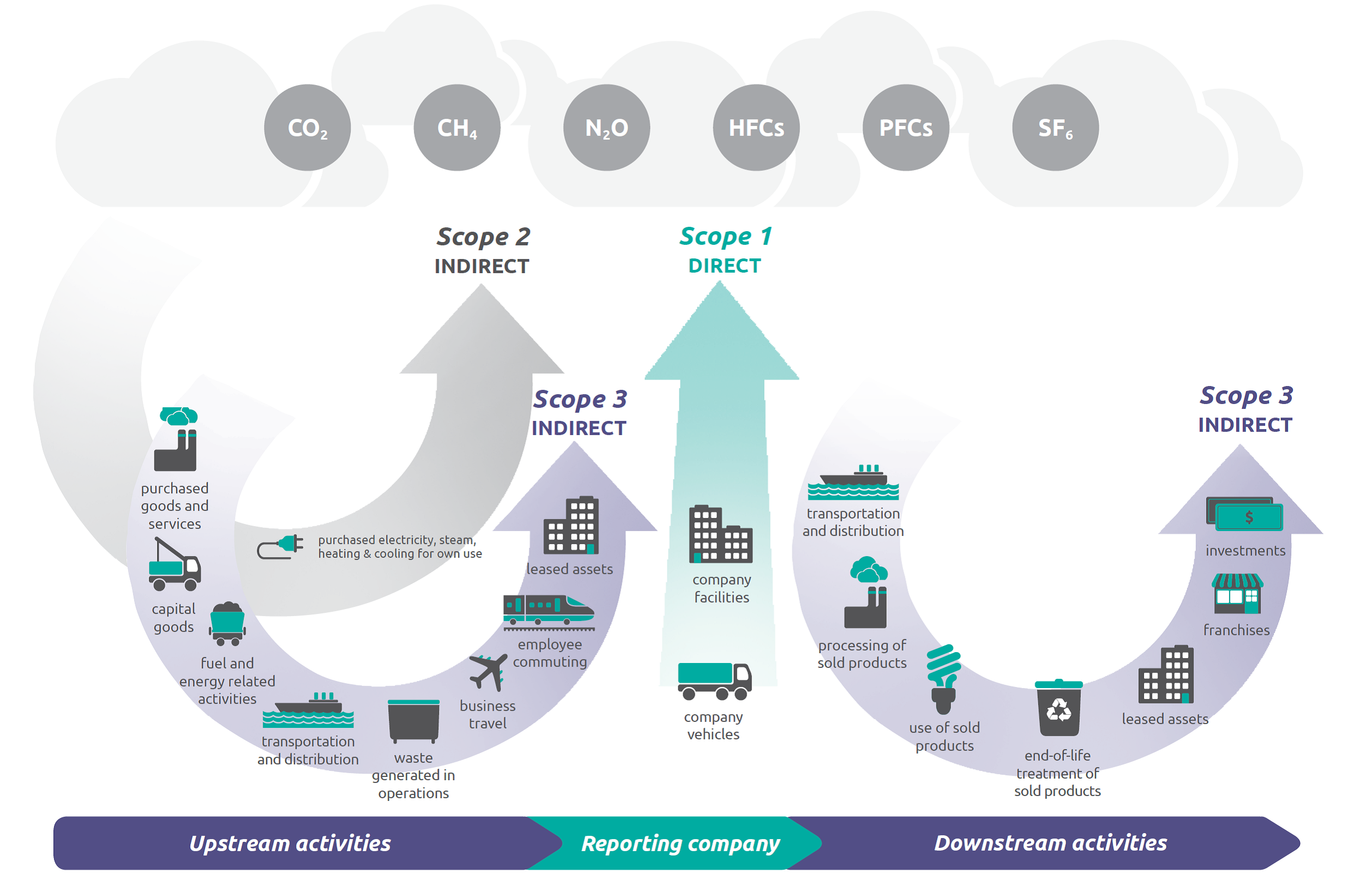

GHG Emissions Across the Value Chain

Scope 1, 2, and 3 emissions are categories defined by the Greenhouse Gas (GHG) Protocol to help organizations measure and manage their greenhouse gas emissions comprehensively:

The above image has been taken from the United States Environmental Protection Agency “Scope 1 & Scope 2 Inventory Guidance” who have stated the original source to be “WRI/WBCSD & GHG Protocol’s Corporate Value Chain (Scope 3) Accounting and Reporting Standard”.

- Scope 1 (Direct Emissions): Are emissions from sources owned or controlled by an organization. They include fuel combustion in company-owned vehicles, onsite energy generation, and emissions from industrial processes. It is divided into four categories: stationary combustion, mobile combustion, fugitive emissions and process emissions. For example, a factory’s gas-powered boilers, air conditioning units or a fleet of company trucks would fall under Scope 1.

- Scope 2 (Indirect Energy Emissions): Are emissions from the generation of purchased electricity, steam, heating, or cooling used by an organization. While these emissions occur at the power plants that generate the energy, they are attributed to the organization using the energy. For instance, emissions associated with the electricity used in office buildings or manufacturing facilities fall into this scope.

- Scope 3 (Other Indirect Emissions): Are all indirect emissions – not included in scope 2 – that occur in the value chain of the reporting company, including both upstream and downstream emissions. In other words, emissions are linked to the company’s operations. Scope 3 includes emissions from suppliers, business travel, employee commuting, product use, waste disposal, and transportation of goods. These are often the hardest to measure but can represent the majority of an organization’s carbon footprint.

- Upstream emissions may include the extraction and production of purchased goods and services, transportation and distribution before the company’s ownership, waste generated during operations, business travel, and employee commuting. Downstream emissions involve the distribution of sold products, the use of those products by consumers, end-of-life treatment, investments, and leased assets.

- Measuring Scope 3 emissions is complex due to their broad and varied nature. It requires close collaboration with suppliers, service providers, logistics partners, and even customers. However, these emissions can represent over 70% of a company’s total emissions, especially in industries such as manufacturing, retail, fashion, food, and technology. Effective management includes conducting lifecycle assessments, engaging suppliers in emission reduction efforts, promoting circular economy practices, and encouraging product designs with lower environmental impact. Tackling Scope 3 emissions is not just a regulatory or reputational requirement—it’s a strategic step towards building a resilient, low-carbon business model aligned with global sustainability goals.

Note: Currently, Scope 4 & 5 Emissions are Not a Part of the GHG Protocol

- Proposed Scope 4 (Avoided Emissions): Informally used to capture avoided emissions (sometimes called “positive” or “beneficial” emissions), e.g., emissions savings from selling high‑efficiency products. Avoided emissions mean the reductions that can be achieved by making conscious choices in products, services, or processes. Scope 4 measures the lifecycle impact of actions that avoid emissions. Some examples include:

- Using clean renewable energy sources by installing solar panels, windmills, etc.

- Transitioning from internal combustion engines to electric vehicles.

- Upgrading to more efficient equipment.

- Opting for public transport or recycling.

- Protecting forests to sequester carbon.

Scope 4 also reveals hidden emissions in specific industries:

- Marketing: Emissions linked to increased demand driven by advertising.

- Legal: Emissions associated with advising high-carbon industries.

- Consulting: Impacts of guidance enabling resource-heavy activities.

- Design: Emissions locked in by material and process decisions.

- Proposed Scope 5 (Created Emissions): These emissions (also dubbed “created” or “negative externality” emissions) cover:

- Inefficient products: Appliances designed to be less efficient or deliberately unrepairable—e.g., top‑load washing machines that use 25–50% more energy than comparable models.

- Planned obsolescence: Business models encouraging frequent replacement rather than longevity.

- Regulatory evasion: Efforts to weaken or skirt climate regulations (such as the auto industry’s marketing push to reclassify vehicles as “light trucks” to avoid stricter fuel‑economy standards).

- Lobbying & disinformation: Activities that slow down or obstruct broader climate action—funding climate‑denial groups, political lobbying against emissions standards, or public campaigns that muddy the scientific consensus.

This approach aims to capture a company’s negative contributions over time, discouraging greenwashing by holding firms accountable not just for emissions they directly report, but also for the additional climate harm caused by their broader behavior.

The above has been taken from an article by Ivy Byrd on the Medium titled “Is it Time for Scope 5 Carbon Emissions?” published on 25 January 2024.

What is the Relevance of GHG Emissions to Sourcing & Procurement, Manufacturing, Supply Chain & Logistics Operations?

GHG emissions are critically relevant because they encourage responsible, ESG-integrated, sustainable and circular operations, while directly influencing environmental sustainability, regulatory compliance, corporate social responsibility, and triple bottom line business performance. Managing these GHG emissions is essential for mitigating climate change and aligning with global sustainability goals.

GHG emissions are critically relevant because they encourage responsible, ESG-integrated, sustainable and circular operations, while directly influencing environmental sustainability, regulatory compliance, corporate social responsibility, and triple bottom line business performance. Managing these GHG emissions is essential for mitigating climate change and aligning with global sustainability goals.

Responsible Procurement: Procurement decisions significantly impact an organization’s carbon footprint. By sourcing materials with lower embedded GHG emissions, such as recycled or sustainably produced goods, companies can reduce upstream Scope 3 emissions. Partnering with suppliers committed to sustainable practices and requiring transparency in emissions reporting also fosters accountability and drives emission reductions across the supply chain.

Sustainable Manufacturing: Manufacturing is often a major source of Scope 1 and 2 emissions from energy use and industrial processes. Implementing energy-efficient technologies, switching to renewable energy, and optimizing waste management can lower emissions and operational costs. Furthermore, designing products with sustainability in mind—reducing resource intensity and enabling recyclability—ensures lower lifecycle emissions. Compliance with increasingly stringent environmental regulations, such as carbon taxes or emissions trading schemes, is also vital to avoid legal and financial risks.

Circular Supply Chain Operations: A significant portion of emissions often arises from global supply chain activities, including transportation, logistics, and distribution. Optimizing routes, transitioning to low-carbon transportation methods, embedding circularity and engaging suppliers in emission reduction initiatives are crucial for managing Scope 3 emissions.

How do major global ESG reporting frameworks & disclosure standards differ in their approaches?

Major global ESG reporting frameworks and disclosure standards differ in scope, focus, and target audience, illustratively:

- SASB (Sustainability Accounting Standards Board) – Focuses on financially material ESG issues specific to industries, targeting investors.

- GRI (Global Reporting Initiative) – Emphasizes broader stakeholder impact and double materiality, covering social, environmental, and economic topics.

- GRESB (Global Real Estate Sustainability Benchmark) – Specializes in real assets (real estate and infrastructure), focusing on ESG performance benchmarking.

- TCFD (Task Force on Climate-related Financial Disclosures) – Provides climate-related financial risk disclosures around governance, strategy, risk management, and metrics.

- TNFD (Taskforce on Nature-related Financial Disclosures) – Like TCFD but focused on nature and biodiversity-related risks and opportunities.

- CDP (Carbon Disclosure Project) – A disclosure system focused on environmental data such as climate change, water security, and deforestation.

- GHG (Greenhouse Gas) Protocol – Sets the standard for measuring and managing greenhouse gas emissions, forming the basis for many other frameworks.

- PCAF (Partnership for Carbon Accounting Financials) – Provides methodologies for financial institutions to measure and disclose GHG emissions from loans and investments.

- SBTi (Science Based Targets initiative) – Guides companies in setting emissions reduction targets aligned with climate science.

What strategies can corporations adopt to align with these evolving ESG ecosystems?

To align with evolving ESG ecosystems, corporations should start by conducting a materiality assessment to identify the most relevant ESG issues. Integrating ESG into core strategy, governance, and risk management is crucial. Companies should adopt robust data collection systems for emissions, supply chains, and social impact, and ensure transparency through consistent, verifiable reporting. Engaging stakeholders early and regularly helps refine priorities. Finally, businesses can set science-based targets and align with global standards like the GHG Protocol and SBTi to demonstrate genuine climate action.

Corporate Sustainability Reporting Directive (CSRD)

The Corporate Sustainability Reporting Directive (CSRD) is a European Union regulation aimed at enhancing and standardizing sustainability disclosures by companies operating in the EU. Replacing the earlier Non-Financial Reporting Directive (NFRD), the CSRD significantly expands the scope, depth, and consistency of corporate sustainability reporting.

Effective from January 1, 2024, large EU companies and listed SMEs (with phased-in deadlines through 2028) are required to report detailed information on environmental, social, and governance (ESG) matters. This includes disclosures on climate risks, social impact, human rights, and corporate governance, using the European Sustainability Reporting Standards (ESRS) developed by EFRAG.

A key feature of the CSRD is its emphasis on double materiality—requiring companies to report not only how sustainability issues affect their business, but also how their activities impact people and the environment. Reports must be digitally tagged and assured by external auditors for greater transparency and comparability.

The CSRD aims to make sustainability reporting as important and reliable as financial reporting, enabling investors, consumers, and stakeholders to make informed decisions. Companies outside the EU that have significant operations within it may also fall under its scope, making it a transformative regulation with global implications for corporate accountability and climate action.